Non-Imagery EO Data: Golden Ticket or Pipe Dream?

The landscape for Earth Observation (EO) markets is growing with new satellite operators entering the market and thus offering more and more data. As players with a foothold in the industry cater to demand for optical and SAR data, new non-imagery data operators are emerging to more choices with hyperspectral, thermal infrared (TIR), radio occultation (RO), Automatic Identification Services (AIS), radiofrequency (RF) monitoring, and microwave sensing (MW) datasets.

This non-imagery data adds new dimensions to help solve customers’ problems they could not address before. This was particularly obvious in the boom that the war in Ukraine created, when this added more power to the EO sector playbook, using these sources as additional elements to other available data, rather than replacing it. But with the oft-heard criticism that there is too much EO data and not enough solutions to solve real customer problems, there are improvements needed on pricing models and data accessibility too for this market. Thus, the overarching question on demand for non-imagery sources in the long-term and the size of the opportunity is still front and center.

A Government Market First

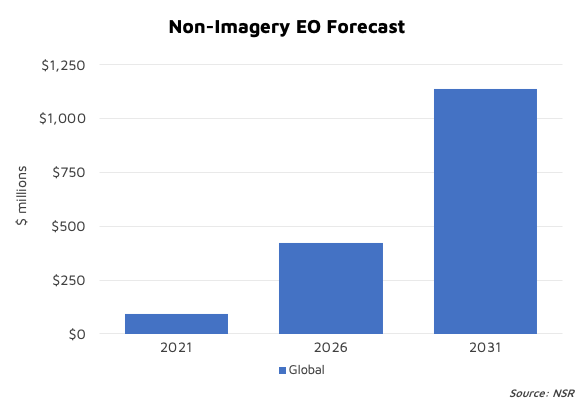

NSR’s Satellite-Based Earth Observation, 14th Edition report shows a total revenue opportunity of $5.4B for non-imagery markets over the 2021-2031 period. Despite having a lower market share compared to optical and SAR imagery, it is the fastest growing EO market at CAGR of 28.7%.

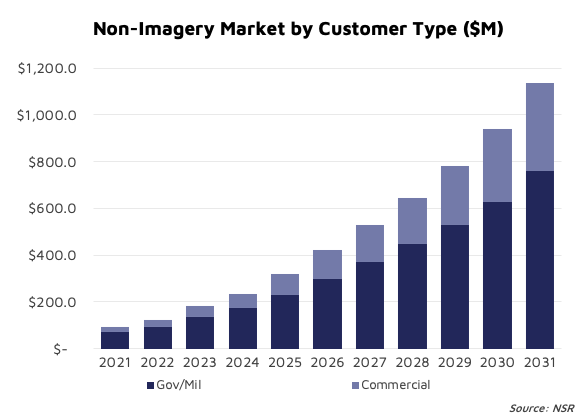

Non-imagery consists of RO, AIS, MW, RF, hyperspectral, etc. and NSR believes it will drive the highest growth across all data types to $1.1 B in 2031, from just above $90 M in 2021. Revenues in the short term are expected to come from government and military clients utilizing (for example) RF monitoring for ISR applications. The NSR forecast is based on this fast adoption road and as a result, sees government revenues will top $761 M at the end of the ten-year forecast.

The market got a recent boost of confidence with the NRO study contracts awarded to Aurora Insight, HawkEye 360 Inc., Kleos Space, PredaSAR, Spire Global and Umbra to assess their commercial RF capabilities and how it integrates with NRO’s architecture to support defense and intelligence communities and policy makers. This is part of a strong push to use of commercial solutions within the U.S. Space Force and NOAA, and it is likely that it will support Gov/Mil customers’ continued lead in generating revenues for this market over the forecast period.

Good for Many Commercial Verticals

Environment, Social and Governance (ESG) applications are another major driver for this segment as the regulations start to kick-in seriously over the next few years. As the world moves towards the ‘net-zero initiatives’, emissions monitoring will be a key use case for these new players. A few of them, like GHGSat and Bluefield Technologies, are focused on carbon and methane emissions monitoring supporting the action to address monitoring climate change. Weather RO data is also critical, especially for maritime applications and Spire has won contracts with Gov/Mil customers (NOAA) and other commercial customers. With proven capabilities of these players to provide the data with higher accuracy, the adoption of these data sets is expected to increase in the long term. In addition to satellite data, the adoption of analytics solutions focusing on niche use cases growing for the non-imagery market but will probably require further acquisition and/or consolidation to leverage all available resources.

Hyperspectral is another key segment in non-imagery market growing swiftly at CAGR of 56.9%. Commercial companies like Pixxel have successfully launched their first satellites in orbit, and this type of imaging, compared to multispectral, can provide additional insights on materials on the surface based on reflectance. Thus, it could play a pivotal role in agriculture, environment, government, energy, and mining applications for use cases such as:

- Agriculture: crop health monitoring, nutrient deficiency detection, detection of variations, improve crop yield.

- Environment: forest monitoring, deforestation, monitoring climate risks, water resource monitoring.

- Government: construction site monitoring; monitor inland waterways, roadways, railroads; mapping, etc.

- Energy: quantify seepages, detect new reserves etc.

- Mining: mineral exploration, mapping ore deposits etc.

More Data, Less Costly

The supply for this type of data is expected to grow with the many planned constellations that will become operational in the coming years, on top of the increase in the number of satellite of current constellations. However, key element of adoption of these data sets will depend on pricing; i.e., if the image acquisition cost is lowered, it could translate to customer paying lower prices and thus engaging more in data procurements. Satellogic, for example, has focused on reducing image acquisition costs with dual payloads on its satellites (high resolution optical and hyperspectral imaging) and distribution of its data through partner Orbital Insights’ platform to “…lower those cost per square kilometer” and “…open up the market”.

IR is another area where use cases such as wildfire monitoring, asset monitoring such as buildings, solar farms, energy transition is laying the foundation for a market that NSR expects will grow to $93M by 2031, based on the use of this data in conjunction with optical and SAR.

And Investors Support Is There

To help with the growth path that many of the new players are entering, there has been lot of support from the investment community recently in this segment, mainly by VCs and Government for the likes of Pixxel, Satellite VU and Muon Space, among others.

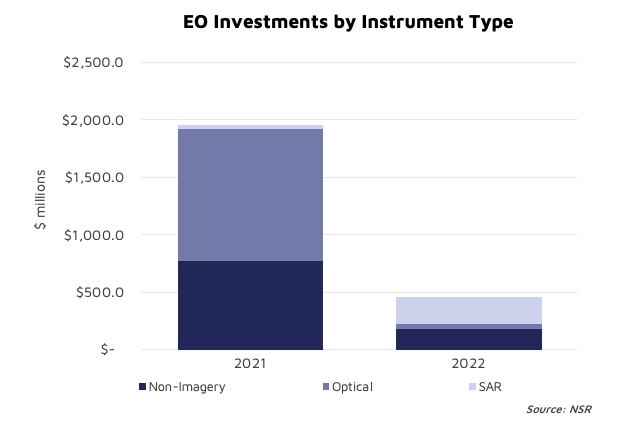

These investments have grown significantly in 2021 and since the beginning of 2022. Last year only, non-imagery investments topped $770 M, second only in EO markets to the optical markets funding. One such deal that shows the thirst of investors is RF data provider Hawkeye-360, which raised $145M in Series-D, a phenomenal amount for a company with 18 cubesats, that will bring its total capital raised to over $300 M.

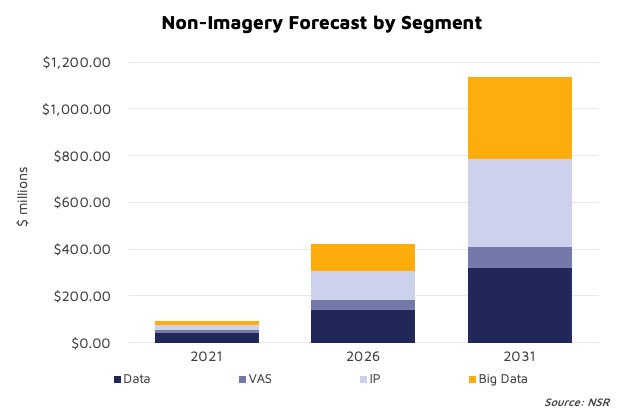

These investments indicate that interest in EO markets diversification is present. Similarly, along other investors, the Government of Canada funded GHGSat for methane emissions monitoring, supporting the sector’s rising awareness of the industry. There is lot of investment in the upstream segment, but in the long-term, the value is expected to shift to downstream services with growing demand for information products and big-data analytics using non-imagery as a data source, with both of these segments forecast to go above $700 M in 2031. It will certainly lead the way for upstream players (operators) who are often satellite manufacturers, to vertically integrate and provide downstream services to expand their addressable market and grow associated revenues.

The Bottom Line

The non-imagery market is a new and emerging trend in EO that has seen successful launches of satellites by commercial satellite operators. However, the data and the ability of operators to gather successful customers is proven mainly in the government segment but with low revenues stream up to now.

Thus, the demand signals for this market are still weak and potentially will increase once the data quality and utility at optimal cost is established by satellite operators and service providers, and beyond their traditional market, with more commercial customers. Despite higher market barriers, demand for the non-imagery market is yet to fully materialize, but it has a very high potential, such that it is neither a ”golden ticket”, nor a “pipe-dream”…at this point.